Press release 02/12/2019

QUARTERLY ACCOUNTS. III/2019

The GDP of the Basque Country rose by 2.1% in the third quarter of 2019

Employment continued to grow, with a year-on-year growth of 1.6% registered in the third quarter

The GDP of the Basque Country was up 2.1% in the third quarter of 2019, compared to the same quarter of the previous year, according to Eustat data. Compared to the second quarter of 2019, estimated growth was at 0.5%.

These increases exceeded the estimates in the Advance Quarterly Economic Accounts for 30 October by one tenth and place the year-on-year variation rate of the Basque Country GDP slightly above most of those of its neighbouring economies.

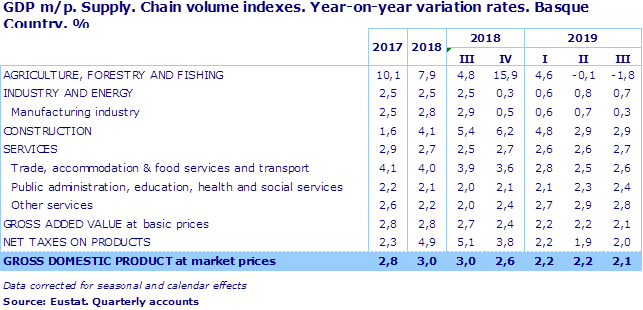

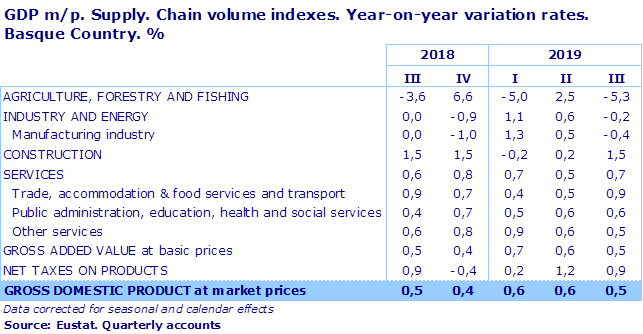

In terms of Supply, analysing changes in the production sectors revealed that the trend of growth in year-on-year rates is widespread across all sectors, except in the Primary Sector (Agriculture, Livestock and Fishing), which was down 1.8% compared to the third quarter of 2018.

The Industry and Energy sector continued a trend of moderate growth observed since the end of 2018, with a year-on-year variation of 0.7%. In fact, this year-on-year deceleration marks a contraction of 0.2% in the sector with respect to the previous quarter. The dynamism of the Manufacturing Industry was weaker than that of the sector as a whole, with a year-on-year growth of 0.3% and a quarter-on-quarter decline of 0.4%.

The Construction sector maintained the growth rate observed in the previous quarter, with a positive rate estimated at 2.9% compared to the same quarter of 2018. In quarter-on-quarter terms, the trend was also positive, growing by 1.5% with respect to the previous quarter (above the more modest 0.2% quarter-on-quarter estimated for the second quarter of the year).

A stronger upward trend to that of the previous quarter was registered in global activity in the Services sector, with a year-on-year growth of 2.7% and a quarter-on-quarter growth of 0.7%. The sub-sector that performed best was Other Services, which encompasses professional, scientific and technical activities, as well as financial and insurance activities, among others. Its value added was up 2.8% with respect to the same quarter of 2018 and up 0.5% with respect to the previous quarter. Both the year-on-year rate and the quarter-on-quarter rate were one tenth lower than those estimated in the second quarter of the year. The Trade, Hotel Management & Catering and Transport sub-sector saw an acceleration in its growth in the third quarter, both in year-on-year terms (an increase of 2.6% compared to 2.5%) and in quarter-on-quarter terms (an increase of 0.9%, four tenths higher than in the previous quarter). Finally, the value added of Public Administration, Education, Health and Social Services was 2.4% higher than the same quarter of the previous year and 0.6% above that estimated in the second quarter of 2019. Year-on-year growth was one tenth higher than that observed in the second quarter whilst quarter-on-quarter growth was identical.

The Gross Added Value at basic prices of the Basque Country (obtained by adding the value added of the production sectors together), in chain volume index terms, saw an increase of 2.1% this quarter compared to the third quarter of 2018, and an increase of 0.5% compared to the second quarter of 2019. Both the year-on-year and quarter-on-quarter variations were one tenth lower than the variations estimated in the previous quarter.

In terms of supply, Gross Domestic Product at market prices, which is obtained by adding Net taxes on products to Added Value, saw an increase of 2.0% in its aggregated value in the third quarter of 2019 compared to that estimated in the third quarter of 2018, and 0.9% compared to the second quarter of 2019.

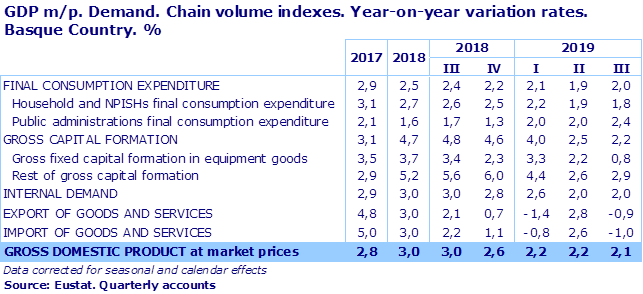

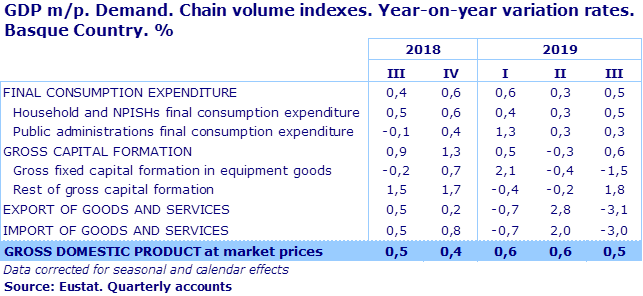

Analysing the estimated change in GDP in terms of Demand reveals that, in year-on-year terms, Internal Demand grew by 2.0%, one tenth less than the GDP. The effect of trends in the foreign sector on the whole economy was therefore slightly positive. Exports of Goods and Services were down by 0.9% in year-on-year terms (3.1% in quarter-on-quarter terms) and Imports of Goods and Services were down 1.0% (3.0% compared to the previous quarter), resulting in a positive year-on-year contribution to GDP of one tenth due to the improvement in the foreign sector balance.

Final Consumption Expenditure of Households (Private Consumption) continued to grow, although at a more moderate rate than in previous quarters. The year-on-year growth rate was 1.8%, also an upturn of 0.5% compared to the previous quarter (two tenths higher than the estimated rate for the previous quarter).

In Public Consumption (Final Consumption Expenditure of Public Administrations), on the other hand, an acceleration of the expenditure was estimated, with a year-on-year increase in the macro-magnitude higher than the second quarter of 2019 (2.4% in the third quarter compared to 2.0% in the second quarter). This implies a quarter-on-quarter growth of 0.3% (identical to that estimated in the previous quarter).

The overall performance of the Final Consumption Expenditure of Public Administrations and the Final Consumption Expenditure of Households led to an upturn of 2.0% in Final Consumption, one tenth higher than the growth in the previous quarter. Compared to the second quarter of 2018, there was an increase of 0.5% (compared to 0.3% estimated in the second quarter).

Gross Capital Formation (Investment) continued the deceleration observed over the last quarters, with year-on-year growth of 2.2%. This implies a quarter-on-quarter variation of 0.6%. The evolution of Investment components has not been homogeneous. Gross Fixed Capital Formation in Capital Goods increased at a considerably slower rate, both in year-on-year terms (0.8% growth) and in quarter-on-quarter terms (1.5% decrease). However, Other Gross Capital Formation, closely tied to the performance of the Construction sector, but which also includes, for example, expenditure on R&D, saw a slight revival of its acceleration, reaching a year-on-year growth of 2.9%. With regards to the second quarter of 2018, this represented an increase of 1.8%, following two quarters of decline.

Regarding changes in GDP by Province, in year-on-year terms, Bizkaia saw a growth higher than the Basque Country overall, with a variation rate of 2.3%. Gipuzkoa grew at the same rate as the Basque Country overall, 2.1%, whilst Álava did so to lesser extent, with an estimated growth of 1.6%. Compared to the second quarter of 2019, these increases imply a growth rate of 0.7% in Bizkaia, 0.4% in Gipuzkoa and 0.3% in Álava.

Employment, measured as full-time equivalent Jobs, continued the upward trend observed in recent periods. In year-on-year terms, growth was estimated at 1.6% (a level of employment 0.4% higher than the previous quarter). This upward trend is due to the creation of jobs in all of the production sectors in relation to the same quarter of the previous year (1.2% in the Primary sector, 0.5% in Industry, 2.3% in Construction and 1.8% in the Services sector). In quarter-on-quarter terms, however, the Primary sector and Industry saw a reduction in the number of jobs (0.3% and 0.1% respectively), whilst there was an increase in the Construction and Services sectors (0.9% and 0.5% respectively).

The evolution in Employment showed a positive performance in the three Provinces. It rose by 1.7% in Bizkaia, 1.6% in Gipuzkoa and, finally, the upturn in Álava was 1.2%. In relation to the second quarter of 2019, Bizkaia also stands out with a growth of 0.5%, compared to a growth of 0.3% estimated for both Gipuzkoa and Álava.

For further information:

Eustat - Euskal Estatistika Erakundea / Basque Statistics Institute

C/ Donostia-San Sebastián, 1 01010 Vitoria-Gasteiz

Press Service: servicioprensa@eustat.es Tel: 945 01 75 62